1. Introduction

As part of the development of Consumer Scotland’s annual Work Programme for 2026-2027, we produced a Draft Work Programme which sets out the key priorities that we intend to deliver in the coming year.

The Draft Work Programme summarises how we intend to work towards the

achievement of consumer outcomes through our priority activities and our

supporting and scoping work.

This work covers a range of sectors, including housing, telecommunications, financial services, energy, heat networks, water and postal services. It also covers our investigations, our work on the Consumer Duty for public bodies, our work on recall of dangerous goods, and our work with key partners to ensure the provision of high-quality consumer advice in Scotland.

We sought formal feedback on the Draft Work Programme as part of our

commitment to delivery, openness and transparency. Drawing from a wide range of relevant knowledge, experience, and perspectives has helped to further inform the refinement of our final Work Programme and ensure that, as Scotland’s independent, statutory consumer body, our work sets the agenda for the consumer landscape and adds value to work of other industry, advice, regulatory and enforcement bodies.

The final Work Programme has been published alongside this document, and laid before the Scottish Parliament.

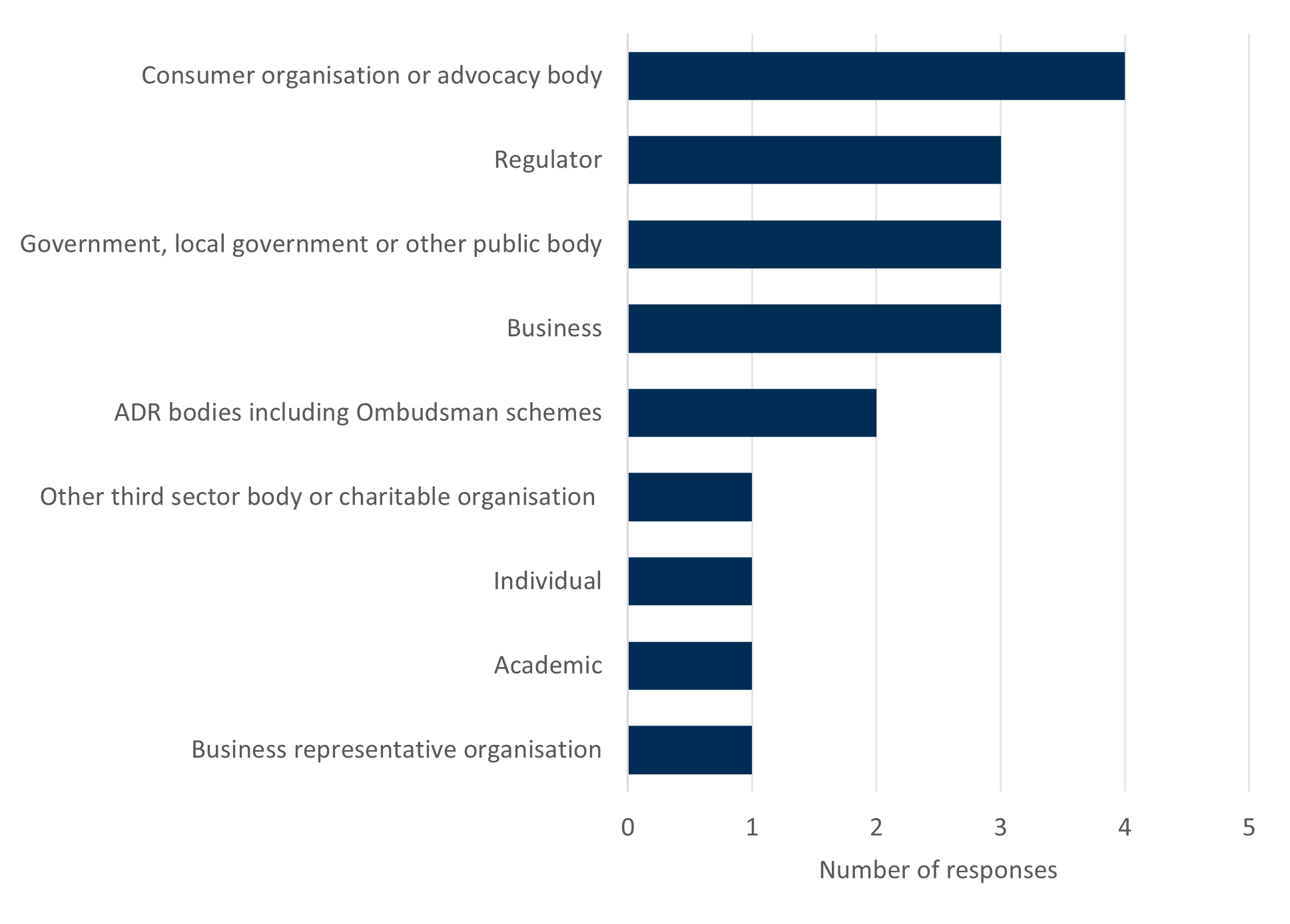

Our consultation period ran for four weeks in January and February 2026. We received 20 formal responses to our consultation from a range of organisations, and one individual (see Chart 1 below). As part of the consultation process, we also held meetings with stakeholders to discuss the Draft Work Programme and our proposed activities and priorities. We are grateful to all those who provided feedback. The organisations that formally responded to the consultation are listed in Appendix 1.

Chart 1: Respondents by category

A range of different types of organisations responded to Consumer Scotland’s consultation on its 2026-27 Draft Work Programme, with consumer organisations the most common.

This document summarises the formal responses to the consultation on our Draft Work Programme for 2026-2027.

Our overarching consumer outcomes received broad support from respondents, and the majority expressed a desire to collaborate with Consumer Scotland in delivering our proposed activities. A number of respondents highlighted the positive working relationship that they already have with Consumer Scotland, and committed to continuing to work closely with us during the year ahead.

As in previous years, a key theme to emerge was the importance of ongoing close collaboration and regular dialogue with stakeholder organisations to avoid any unnecessary duplication of effort. This is feedback we will take on board in 2026-2027, while ensuring that we deliver our remit as Scotland’s independent statutory consumer body.

Many respondents also highlighted relevant activities that may support us in the delivery of our priority activities.

Some respondents also noted that they had previously suggested certain consumer issues for our consideration, prior to the consultation, as part of our ongoing collaboration.

The rest of this document summarises the more specific responses to our Draft Work Programme, structured according to the overarching consumer outcomes that Consumer Scotland is working towards, with reference to their component priority activities. It also includes responses relating to our supporting and scoping work, as well as general comments and recommendations.

2. Consumer Outcome: Reducing consumer harm

Our strategic focus on reducing consumer harm was generally well received, and specific feedback was given across the used cars, housing, water and energy workstreams associated with this consumer outcome.

Used Cars

Our plans to investigate Scotland’s used car market received positive feedback, with one respondent highlighting that “used cars cause some of the biggest and most practical detriment to consumers”. There was also support for our intention to seek clearer, more consistent standards across enforcement and advice, and it was suggested that we extend our focus to include the electric vehicle market, which could be supported by recent studies carried out in this area.

Housing

Respondents commented favourably on our proposed work on “tackling consumer detriment in home improvements”. Respondents noted that our identified themes around consumer detriment reflected insights from their own work on green heating and insulation, alongside wider consumer issues arising in trader recommendation sites.

Respondents also pointed out the potential connections between this outcome with consumer issues around heat networks - including pricing, billing fairness, and complaints handling - and the growing risk of consumer detriment as the market continues to expand. One respondent drew attention to their work on the development of the Heat and Energy Efficiency Technical Suitability Assessment (HEETSA), which includes a focus on heat networks, and were keen to share insights where our workstreams may intersect.

Water

Consultees with a particular interest in the water sector communicated a desire to build on recent and ongoing collaboration with Consumer Scotland. In the context of our proposed work on “supporting vulnerable water consumers”, one respondent drew attention to some of the challenges in comparing the water sector’s Priority Service Register (PSR) with the energy sector, due to the different regulatory requirements and incentives. They highlighted current work to support vulnerable consumers, and suggested that our work in this area should focus on how to further improve the quality of services provided, as well as the number of consumers receiving these.

In relation to our proposed work on “preventing and dealing with water debt”, stakeholders were keen to hear more about the new evidence our research in this area has generated and to learn about our proposals to help tackle long-standing problems that consumers have experienced in this area.

As part of our “tackling water poverty” workstream, our recommendation to increase the uptake of Council Tax Reduction amongst eligible consumers was welcomed by respondents, however one organisation expressed reservations about our recommendation to increase the level of discount currently provided through the Water Charge Reduction scheme, due to issues with how the scheme is targeted and how well it is understood by consumers.

Comparisons with the energy sector were also made in relation to water poverty, with one respondent suggesting we consider adopting more consistent language across our work on energy and water affordability.

Respondents representing the water industry were also keen to draw attention to the cross-subsidies inherent in the structure of household tariffs, and the resulting challenges in providing affordability support without impacting other consumers.

Energy

Respondents expressed support for our focus on “more affordable energy bills”. One respondent referenced this outcome as one of the potential benefits of large-scale expansion, modernisation, and decarbonisation of the electricity grid, which they argued would better meet new domestic and industrial demand, improve energy security, and reduce exposure to volatile fossil fuel prices, ultimately supporting lower energy bills over time.

3. Consumer Outcome: Increasing consumer confidence

In relation to this outcome, respondents provided general support for Consumer Scotland’s recent research delivered with small business consumer groups, which examined their experiences as consumers in 11 different markets. Continued engagement was welcomed to help facilitate a market which works as well as possible for small business consumers.

A range of views were also expressed towards our proposed work on water and postal services.

Water

As part of our focus on “improving consumer outcomes in the non-household water market”, our Draft Work Programme expressed that current arrangements do not always deliver effectively for business consumers.

One response suggested that this problem statement could be reframed to focus on Consumer Scotland’s role in the development of a first Code of Practice for providers in the non-household market to tackle the difficulties experienced by consumers. If framed this way, it was suggested that the focus of our 2026-27 work could then be more explicitly set out in terms of examining the effectiveness of this Code of Practice and practical opportunities to improve its impact for consumers.

Post

Respondents were pleased to see our ongoing monitoring of the impacts of changes to the universal postal service (UPS) and welcomed our continued participation in Royal Mail’s Customer Engagement Forum to represent consumers’ interests.

Our plans to scope and design a “Post Monitor” – to identify gaps and provide evidence of Scottish consumers’ experiences of letters, parcels and post offices, including USO reform implementation – were viewed by one respondent as a promising opportunity to compare their research plans in this area across England and Wales. One respondent drew attention to Ofcom’s existing postal tracker, and highlighted the need to develop the detail of the planned work further, to avoid any unnecessary duplication.

Regarding our planned qualitative research on consumer experiences of navigating the complaints process in the postal system, some respondents were keen to understand more about this work, specifically what stages of the complaints process the work will focus on. It was suggested that further research could explore the likelihood of consumers raising complaints in the parcels market. Another respondent highlighted that careful planning should again be undertaken to avoid duplication with work carried out by others in this area.

4. Consumer Outcome: Improving the consideration of consumer matters by public bodies

Some of the workstreams associated with this consumer outcome are more broad and cross-sectoral in nature, so they typically attracted less feedback than the more market specific workstreams. In addition to general support for our upcoming Consumer Welfare Report, our proposed workstream in relation to water also received some specific comments, which are briefly outlined below.

Water

Respondents were pleased to see updates to our “putting water consumers at the heart of the Strategic Review of Water Charges for 2027-2033” workstream, with one commenting that our deliberative research has contributed to a “very strong foundation of customer research which has informed Scottish Water’s plans for 2027-2033”.

It was asked that we include recognition of the additional stakeholders who

collaborated on this research programme, and the significant volume of work that has been undertaken in the sector to help achieve this outcome.

5. Consumer Outcome: Promoting sustainable consumption

In addition to a general recognition that efforts should be ongoing to promote sustainable consumption, several consultees provided feedback on the water and energy workstreams associated with this consumer outcome.

Water

Our focus on a “water system that responds to climate change” was generally supported, with respondents advocating for collective responsibility in these efforts. One respondent said: “Adapting to climate change requires a systems-based, cross-sectoral and national approach”.

Another respondent advised that in this area, Consumer Scotland should ensure that our advocacy role on policy direction is clear in terms of our positions on particular solutions.

Another consultee expressed that it would be helpful to understand in more detail how we plan to measure the impact of any actions around our work climate change and how our work intersects with relevant work being undertaken by the industry.

Energy

The importance of our focus on “heat networks delivering for consumers” was supported by many consultees, with strong agreement that maintaining consumer confidence in heat networks is critical to increasing the adoption needed to reach current deployment targets. Respondents welcomed our upcoming qualitative research on the sector in Scotland, suggesting collaboration on, and sharing learnings from, their own surveys currently being undertaken.

Respondents also pointed to areas which we may want to investigate further, including the risks to consumers of permitting further development of heat networks where gas is a heat source, due to cases where fuel poor householders have been locked into high tariffs when gas prices have risen sharply.

Another respondent suggested that, in addition to the three key areas highlighted in the Draft Work Programme (fair pricing, reliability, and quality of service) – we extend our focus to protecting vulnerable consumers from disconnection outside of the winter months, and bundled consumers from long-term back billing.

Our proposed work in relation to “access to low carbon technology and advancing energy efficiency” was received positively from a range of respondents. One highlighted similar workstreams being undertaken in England and Wales around EPC reform, minimum energy standards, and the alignment of future advice services for retrofit with existing statutory advice provision. This was seen as an opportunity for continued engagement to ensure best practice in these areas across the UK.

One respondent noted the potential for solar PVs and battery storage to form part of an additional workstream, and offered their support with guidance for consumers. It was suggested that we consider the benefits that consumer protection, advice, and information around the purchase and installation of solar panels and battery storage can provide to consumers, in the form of lower bills, income from grid exports, and improvements to home energy efficiency and EPC ratings. In addition, we were advised to consider consumer information on access to government financial support

for solar and battery storage home improvements.

6. Consumer Outcome: Advancing inclusion, fairness, prosperity and wellbeing

Several consultees provided specific feedback on the telecommunications, energy and water workstreams that are associated with this consumer outcome.

Telecommunications

In relation to our proposed work on “fast, affordable and reliable

telecommunications”, respondents suggested a range of consumer issues relevant to our work. One such concern was that consumers currently receive inconsistent levels of redress and they therefore suggested support for a ‘single ombudsman model’ - as is seen in the energy sector - which can “take a holistic view of sector data and provide sector-wide insights into consumer detriment”.

One consultee, responding as an individual, requested that the negative impacts of the switchover to digital landlines be more explicitly highlight within our Draft Work Programme. They stressed that these changes could disadvantage users in areas where access to digital services is limited, particularly older people and those with health issues, and that outages could prevent people from accessing critical communications, including emergency services.

Energy

Respondents welcomed our focus on “reduced electricity distribution charges” and were keen to view the results of our analysis to better understand our proposed changes to the way charges are recovered.

Referencing the high distribution charges faced by consumers in the north of Scotland, one respondent emphasised the need for long-term investment in the network to maintain system reliability, support future demand, enable the transition to clean power, and ultimately protect consumers from higher costs in the long run.

While most respondents were supportive of our plans around “accelerating the roll out of smart meters”, some shared concerns around potential delays to the roll out, and the need for greater collaboration to establish a consensus on which policies could help realise the consumer benefits they offer.

One individual challenged our support for smart meters in general, drawing attention to issues around their accuracy.

Regarding “a future energy retail market that works for consumers in Scotland”, one respondent encouraged working together to identify areas of concern and opportunities, potentially through the development of universal principles for all energy consumers in the retail market, or by addressing specific barriers faced by consumers, including vulnerable groups and those using pre-payment meters.

Another respondent suggested we consider the key challenges, opportunities and risks that Artificial Intelligence presents for this market, referring to a recent collaboration between the Energy Ombudsman and Ofgem which explored these areas.

Water

In relation to our proposed work on ‘strengthening the evidence base on the issues that matter for water consumers’, respondents with a particular interest in the water sector sought greater clarity on what the ‘strengthening’ activity would look like in practice, and how our statutory role interacts with the interests of relevant stakeholders. One respondent suggested that the final Work Programme should include more detail on the research and activity currently being carried out by the industry to understand and act upon consumers’ needs and expectations.

Regarding the design and implementation of a new consumer survey to gather representative data on attitudes, experiences, and needs, one respondent requested more information on how our work will intersect with key sector decision-making processes.

7. Supporting work and scoping projects

Some of our planned activities that do not constitute priority workstreams for 2026-2027, but are indicative of our longer-term strategic objectives, were addressed by respondents, and received positive feedback.

Respondents were pleased to see our continued membership of the Independent Consumer Panel for legal services, in which we will work alongside partners to optimise the impact of its revised remit and secure the effective implementation of the Regulation of Legal Services Act. They were also supportive of Consumer Scotland’s previous efforts as a “significant voice in advocating for consumer focus in the debate on legal services regulation to ensure that new legislation delivers for consumers”.

Regarding our plans to monitor the data provided to us by Post Office Ltd on the post office network, including location, type of branch, and business mix, one respondent highlighted the need to protect the post office customers most reliant on the network. Another respondent noted the importance of the postal levy only being used on the postal services aspect of this work.

8. General comments and recommendations

Overall, respondents were very supportive of the overarching outcomes set by Consumer Scotland, and the workstreams that will enable us to work towards achieving these.

Respondents frequently highlighted that their organisations had identified similar strategic themes, which offered a strong basis for collaboration.

We also received some suggestions on specific areas to which we could contribute that are not set out in the Draft Work Programme. These suggestions are summarised below.

Improving outcomes for consumers in the postal sector

Suggestions included drawing on cross-sector experience in the design of social tariffs to address the impacts of the cost of living crisis, and advising on the design of a stamp discount scheme, including how to ensure customers that face postal affordability concerns use a scheme. It was also suggested that we would have the resources to promote a stamp discount scheme, including potentially by raising awareness through the advice services that we fund.

Power of Attorney issues

One respondent drew attention to the eight million registered power of attorneys in the UK, and the support they provide for financial services, mobile phone contracts, insurance, utilities, and managing contracts where an individual may not be able to.

They argued that where an individual has been chosen to navigate these markets on behalf of someone else, they should be treated as if they were the consumer. They raised the issues that they face around digital access, accessing financial services, barriers to better interest rates, and routes to redress.

Given the “sparse” data available for power of attorneys in Scotland, it was

suggested that we explore these issues and share our insights in upcoming projects to help gather evidence about the problems power of attorneys face, identify potential changes and improvements, and advise on how best to engage with consumer advocates in Scotland for similar input.

9. Annex A: List of formal respondents

Advertising Standards Authority (ASA)

Advice Direct Scotland

Citizens Advice

Competition and Markets Authority (CMA)

Consumer Council for Northern Ireland

The Fairbanking Foundation

Glasgow Caledonian University & Common Weal

Independent Customer Group (ICG)

National Energy System Operator (NESO)

The National Federation of SubPostmasters (NFSP)

Royal Mail

Scottish Environment Protection Agency (SEPA)

Scottish Legal Complaints Commission

Solar Energy Scotland

Scottish & Southern Electricity Networks (SSEN) Distribution

Scottish & Southern Electricity Networks (SSEN) Transmission

Scottish Water

Trust Alliance Group

Water Industry Commission for Scotland (WICS)